Following along? Install the extension first

Finmagine AI Advisor — free • no account needed • Chrome, Edge, Brave

📚 Multimedia Learning Hub

Master the 7-dimension Deep Analysis framework through video, audio, and interactive flashcards

What You Will Learn

This article is a complete walkthrough of the Deep Analysis template in Finmagine AI Advisor v2.14.0 — the most comprehensive of the three mutual fund templates. It covers all 7 dimensions the AI evaluates, with PPFAS Flexi Cap Fund (VRO fund ID 19701) as the worked example throughout.

The 7 Dimensions Covered:

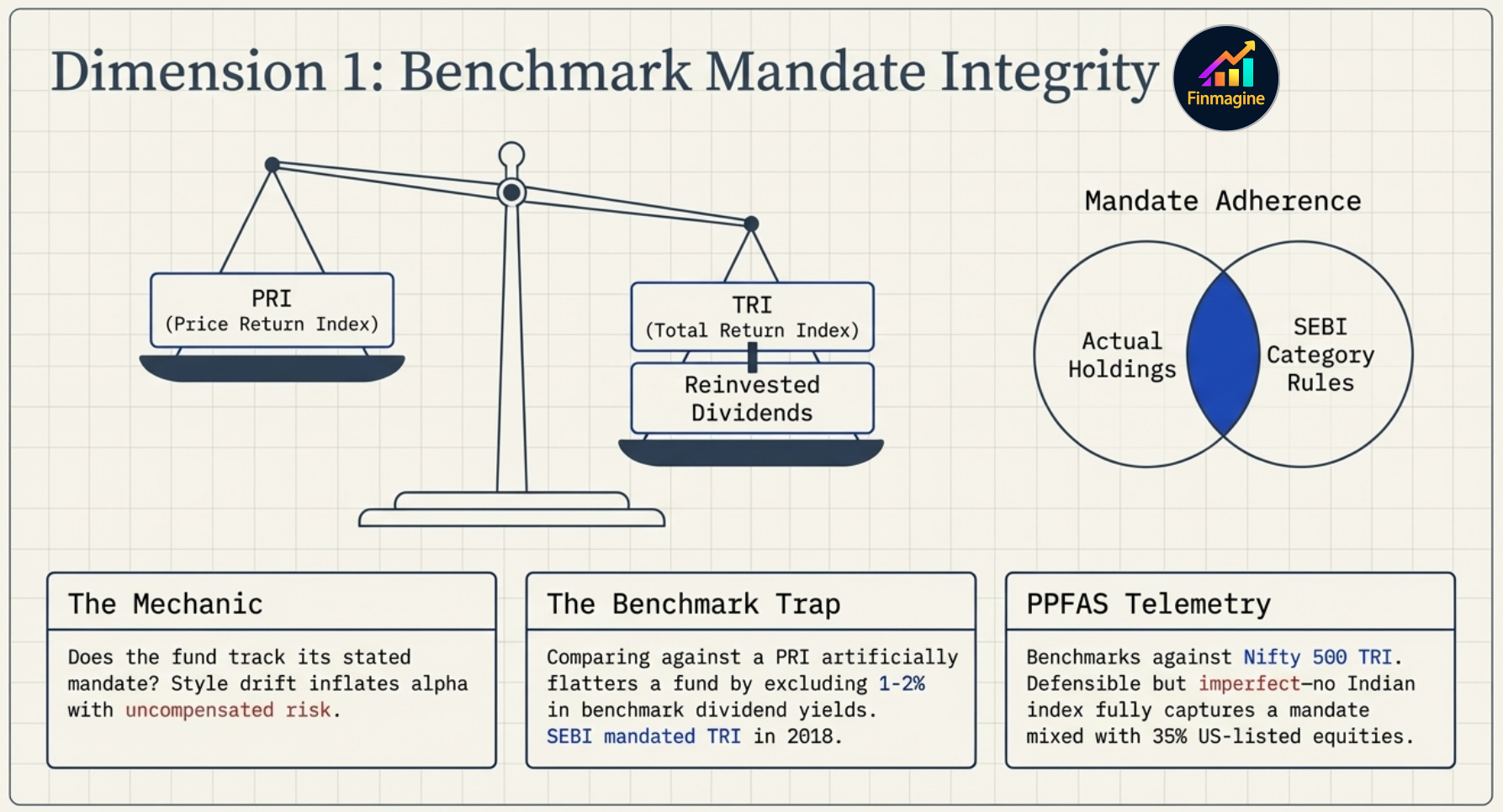

- Dimension 1 — Benchmark Mandate Integrity: Is the fund invested where it claims? Is the benchmark fair (TRI not PRI)?

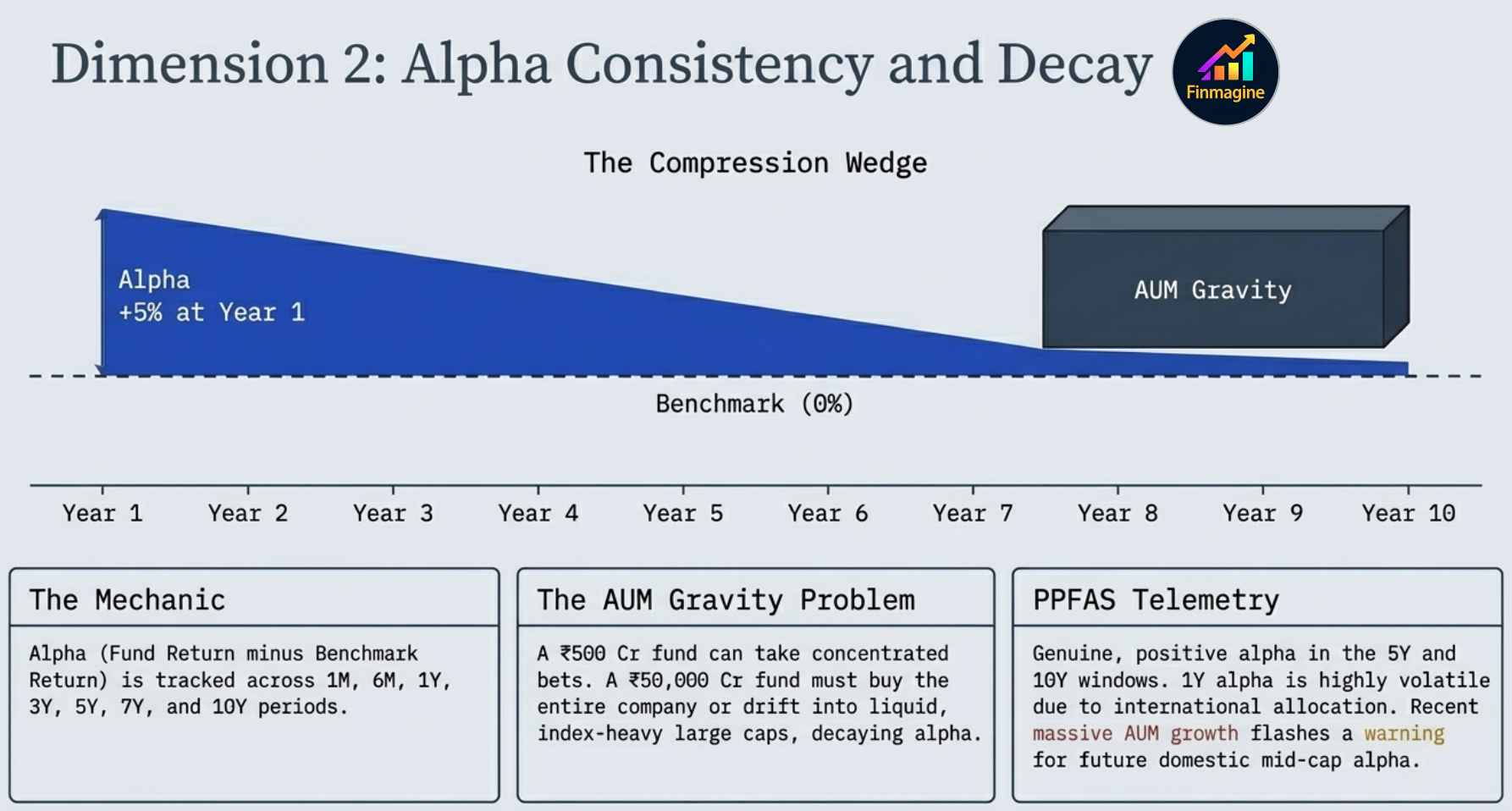

- Dimension 2 — Alpha Consistency and Decay: Does outperformance hold across all 8 time periods, or does it fade as AUM grows?

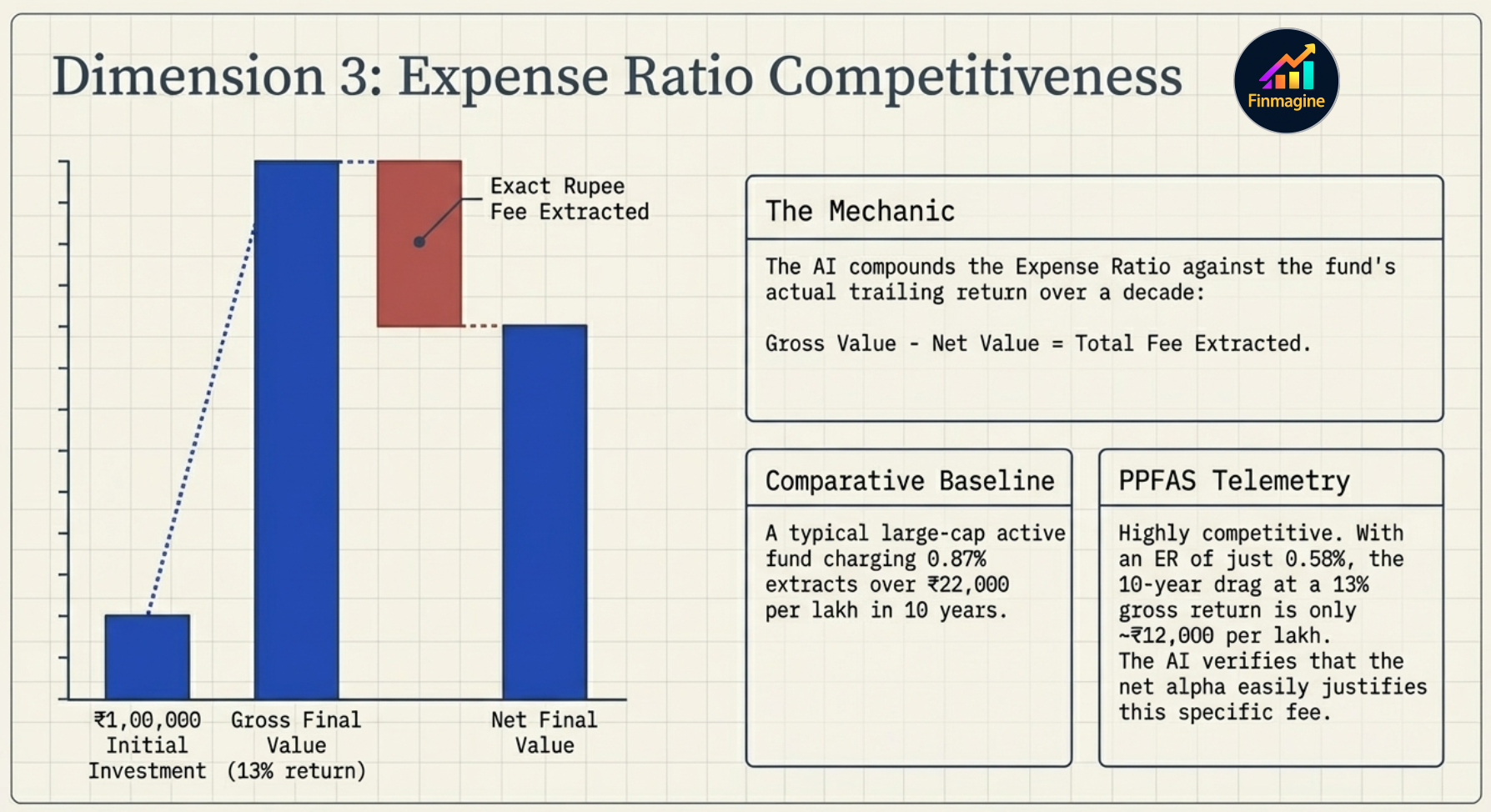

- Dimension 3 — Expense Ratio Competitiveness: 10-year compounded rupee cost drag — the number that makes abstract percentages real

- Dimension 4 — AUM Suitability: Has fund size grown to the point where strategy execution is impaired?

- Dimension 5 — Portfolio Construction Quality: Do the top holdings reflect the stated mandate, or is it closet indexing?

- Dimension 6 — Return Consistency vs Category: First quartile consistently, or random quartile rotation?

- Dimension 7 — SEBI Suitability Verdict: Suitable / Conditionally Suitable / Not Suitable — with explicit conditions

Watch: The Hidden Truth About Mutual Funds (You're Losing More Than You Think)

A deep dive into how mutual funds actually work — and what they don't want you to notice. Uses the PPFAS Flexi Cap Fund case study to walk through the 7-dimension framework.

Topics: Why benchmark comparisons were misleading for years · Alpha decay and how it kills performance · How fund size (AUM) destroys returns · The true cost of a 0.87% fee over 10 years · Why 5-star ratings don't guarantee future returns.

Why Star Ratings Aren't Enough

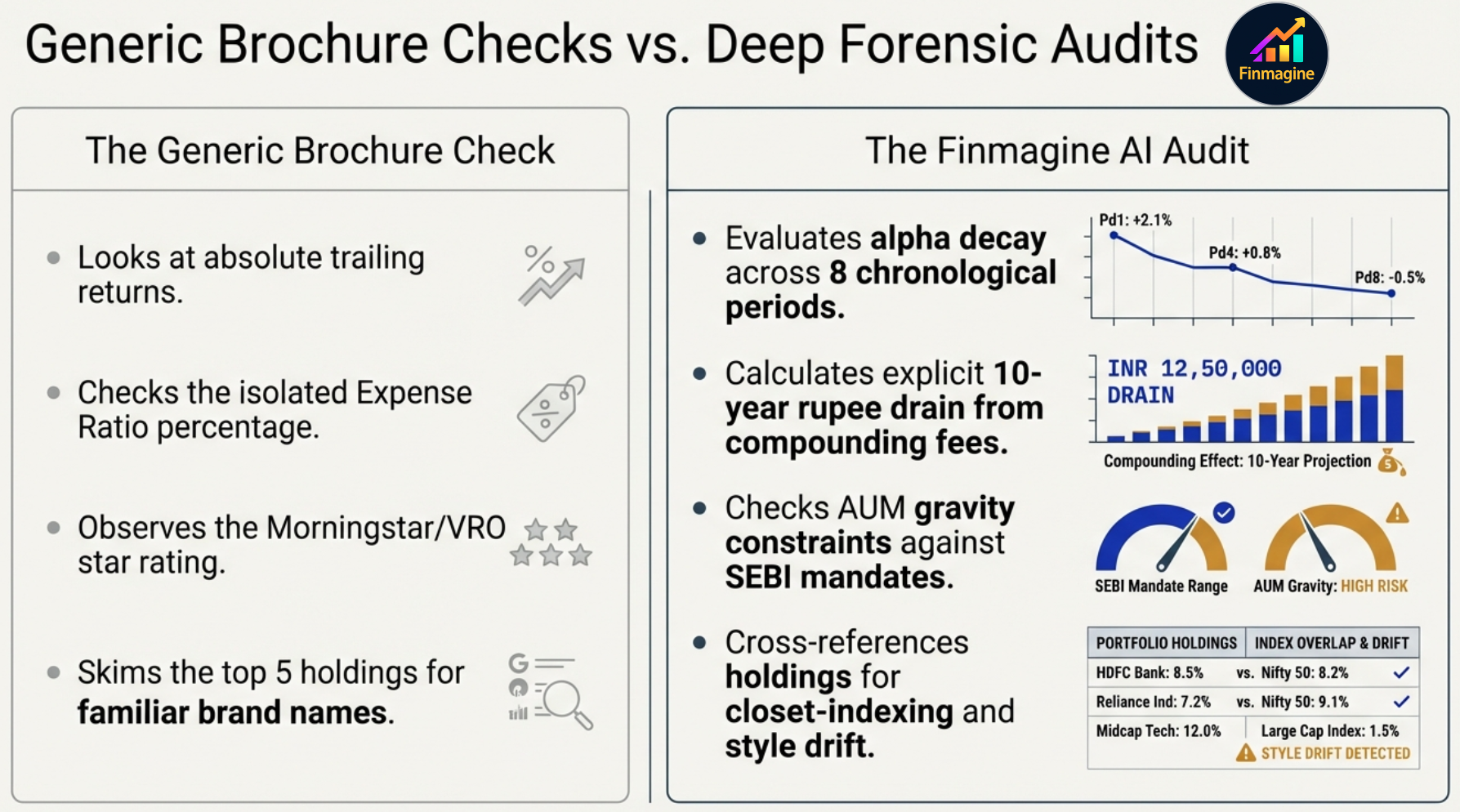

The standard brochure check looks at the surface. The 7-dimension forensic audit goes under the hood.

Every mutual fund fact sheet is a masterpiece of selective disclosure. The five-star badges, the beautiful line chart that only ever goes up-and-to-the-right, the star fund manager profiled in financial magazines — they are all carefully curated to guide you toward one conclusion: buy this fund.

The problem is not that the data is false. It is that the data shown is the data that flatters. Absolute trailing returns sound impressive in a bull market — every fund goes up. A 0.87% expense ratio looks negligible in isolation. AUM growth signals success to the retail investor while it quietly destroys the fund's ability to generate alpha.

❌ The Generic Brochure Check

- Looks at absolute trailing returns

- Checks the isolated Expense Ratio %

- Observes the Morningstar / VRO star rating

- Skims the top 5 holdings for familiar names

✅ The Finmagine AI Forensic Audit

- Evaluates alpha decay across 8 chronological periods

- Calculates the explicit 10-year rupee drain from compounding fees

- Checks AUM gravity constraints against SEBI mandates

- Cross-references holdings for closet-indexing and style drift

The Deep Analysis template does not read the brochure. It reads the evidence — the actual holdings, the actual returns against the correct benchmark, the actual AUM trajectory — and applies a structured 7-dimension framework to produce a verdict no marketing department can pre-approve.

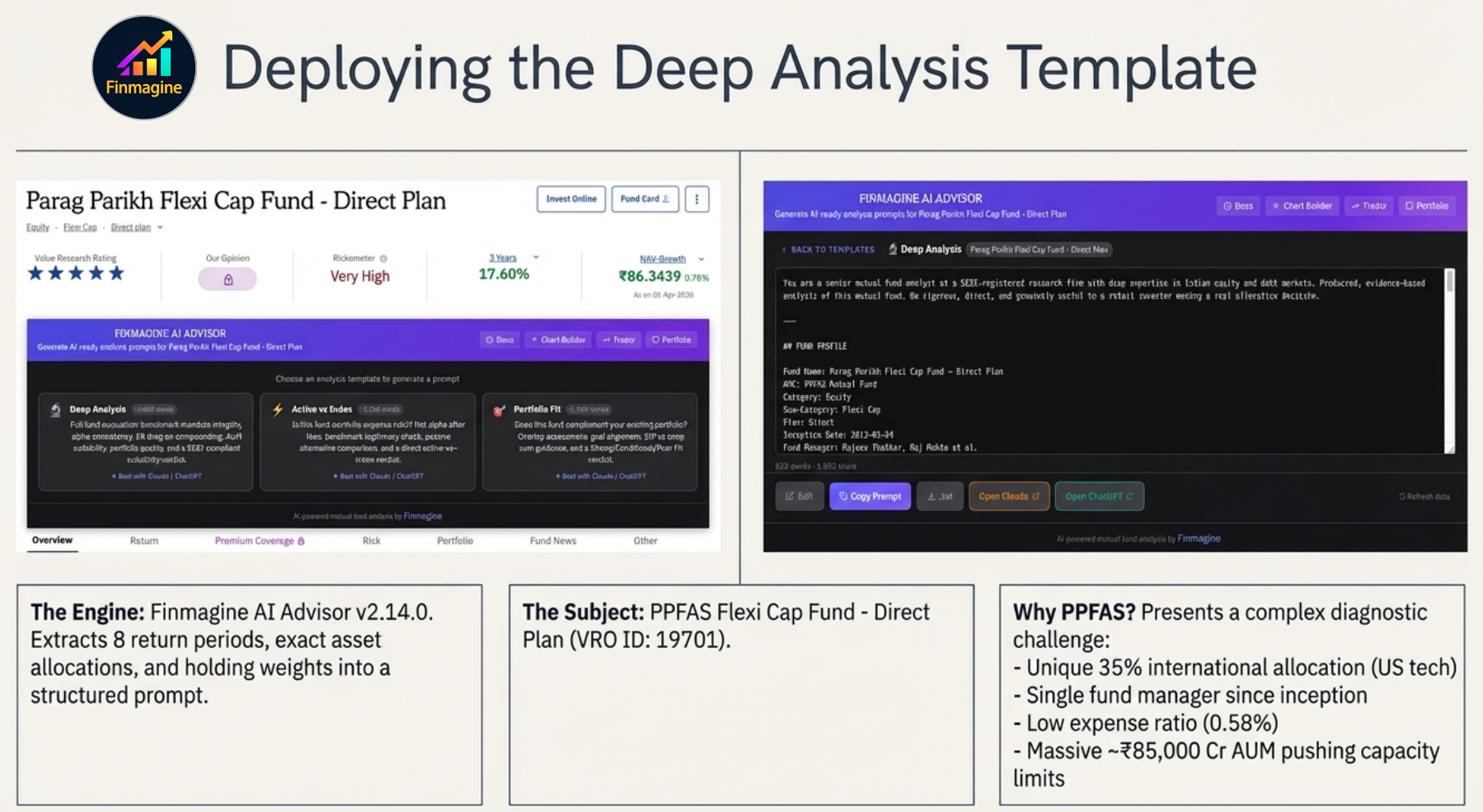

Before You Run the Template

The Finmagine AI Advisor panel on the PPFAS Flexi Cap Fund page — Deep Analysis selected, prompt assembled, ready to copy.

Open any VRO fund detail page. The Finmagine AI Advisor panel appears within 3–4 seconds. Click Deep Analysis, wait a moment for the prompt to assemble, then click Copy Prompt. Paste into Claude or ChatGPT.

The panel embedded on the PPFAS VRO page — three templates available, Deep Analysis selected.

The generated Deep Analysis prompt — ~1,800 words of structured financial context, all populated automatically from the VRO page data.

The 7 Dimensions — Explained

The benchmark trap: a PRI comparison flatters every fund by 1–2% annually. SEBI mandated TRI from 2018 — but the AI still verifies compliance.

This dimension has two sub-checks. First, mandate adherence: does the portfolio's actual composition match its SEBI category? A fund categorised as "Large Cap" must maintain at least 80% in large cap stocks. The top 10 holdings and market cap breakdown are the evidence — not the marketing brochure.

Second, benchmark legitimacy. For decades, mutual fund managers compared their dividend-collecting funds against a Price Return Index (PRI) that conveniently excluded dividends from its calculation. If a stock stays flat but pays a ₹5 dividend, the PRI records 0% growth while the fund's NAV rises. This manufactured 1–2% annual outperformance was entirely fabricated — winning a foot race by making your opponent run in concrete shoes. SEBI ended this in January 2018 by mandating Total Return Index (TRI) benchmarks. The AI verifies full compliance.

The compression wedge: alpha generated at ₹500 Cr AUM cannot survive at ₹50,000 Cr — the fund becomes too large to execute the trades that built the track record.

Alpha is fund return minus benchmark return for each period. The Deep Analysis template computes this across all 8 available periods (1M, 3M, 6M, 1Y, 3Y, 5Y, 7Y, 10Y) and hunts for two patterns:

- Consistency: Is alpha positive across most periods — or concentrated in one lucky window?

- Decay: Does alpha narrow as the time period lengthens? A yellow flag: 1Y alpha > 3Y alpha > 10Y alpha, narrowing toward zero as AUM grew.

The silent wealth killer: a 0.87% ER extracts ₹23,000 from a ₹1 lakh investment over 10 years — nearly 23% of original capital, compounded away in daily fee deductions.

The mutual fund industry has done a masterful job framing the expense ratio as a triviality. You see "0.87%" and your brain categorises it as less than 1% — spare change. But this psychological abstraction conceals the destructive power of compound interest working in reverse. The Deep Analysis template shatters the illusion by translating the percentage into a concrete rupee figure:

The AI then asks the brutal follow-up: does the alpha in Dimension 2 exceed this cost? If the manager generated ₹10,000 of excess return but the fund house extracted ₹23,000 in fees, the investor subsidised the fund manager's office while their own wealth was drained.

Category-specific capacity thresholds — PPFAS at ₹85,000 Cr sits in the conditional warning zone for flexi/large cap funds.

| Category | Capacity Concern Threshold | Structural Impact |

|---|---|---|

| Small Cap | ₹5,000 Cr+ | Market impact cost destroys trade economics; style drift into mid/large cap inevitable |

| Mid Cap | ₹20,000–50,000 Cr | Forced into large caps to deploy cash; mandate drift begins |

| Large Cap / Flexi Cap | ₹60,000–80,000 Cr+ | Closet indexing risk — only Nifty heavyweights are liquid enough to absorb inflows |

| Index Funds / ETFs | No practical limit | Passive execution benefits from scale; AUM irrelevant |

PPFAS's distinctive non-index portfolio — domestic defensives (Bajaj, Coal India, ITC) alongside US tech giants (Alphabet, Meta, Amazon) — signals a deliberate value-oriented barbell thesis, not closet indexing.

The AI does not read the fund's marketing materials. It reads the actual stock tickers and checks for three things:

- Mandate coherence: Does the asset allocation (equity/debt/cash %) match the category mandate? Does the market cap breakdown fit?

- Concentration: Top-3 holding weight between 25–35% signals conviction without recklessness. Above 50% is hyper-concentration risk. Index-like holdings (top 10 = Nifty 50 heavyweights in market-cap order) signal closet indexing.

- Thesis clarity: Do the holdings tell a consistent story? A fund holding Coal India and Alphabet alongside each other looks bizarre — until you recognise the barbell thesis: high-cashflow defensive value anchors + high-growth technology optionality. Coherent. Not random.

PPFAS's quartile journey: volatile in the short term (1Y, 3Y) due to INR/USD dynamics, but locked into the top quartile over 5Y and 10Y — the AI reads this as structural, not a skill failure.

Absolute returns are a mirage created by macroeconomic tides. A rising tide lifts all boats. A completely incompetent fund manager can generate 15% in a year where the broad market surged 25% — and that is a catastrophic failure, not a victory, masked by bull market momentum.

Category rank strips away the noise. The AI classifies consistency using quartile position across all available periods:

| Pattern | Interpretation |

|---|---|

| Top quartile (rank ≤ 25%) across 5Y, 7Y, 10Y | Genuine consistent outperformer — dynasty-level skill |

| Top half consistently but not always top quartile | Solid, reliable — not exceptional |

| Top quartile in one period, bottom half in others | Cyclical or lucky — not a repeatable system |

| Bottom quartile across most periods | Chronic underperformer — active fees unjustified |

All 6 preceding dimensions feed into the AI processing engine to produce one of three SEBI-aligned verdicts — no ambiguity, no brochure-speak.

The final dimension synthesises all six preceding analyses into one of three verdicts. The AI is explicitly instructed to never use generic broker terminology — no "buy", no "sell", no "hold". The verdicts are diagnostic, not prescriptive:

The fund passes most or all dimensions. Benchmark is fair (TRI), alpha is genuine and consistent, expense ratio is competitive, AUM does not impair the strategy, portfolio is well-constructed with a clear thesis, returns are consistently top-quartile. Appropriate for investors matching the fund's stated risk profile and minimum time horizon.

The fund is fundamentally sound but carries specific friction points. The verdict includes explicit conditions — e.g. "Suitable only for investors with a 7+ year horizon who accept that the 35% international allocation will cause 1–3 year underperformance vs India-only peers during periods of INR strength or US market correction." Conditions are stated, not implied.

The fund fails on enough dimensions — negative net alpha after fees, AUM-paralysed strategy, manipulated PRI benchmark, or chronic quartile underperformance. The AI provides a mathematical autopsy: which dimensions failed, with specific numbers cited as evidence. It refuses to use vague language; every disqualification is traceable to data in the prompt.

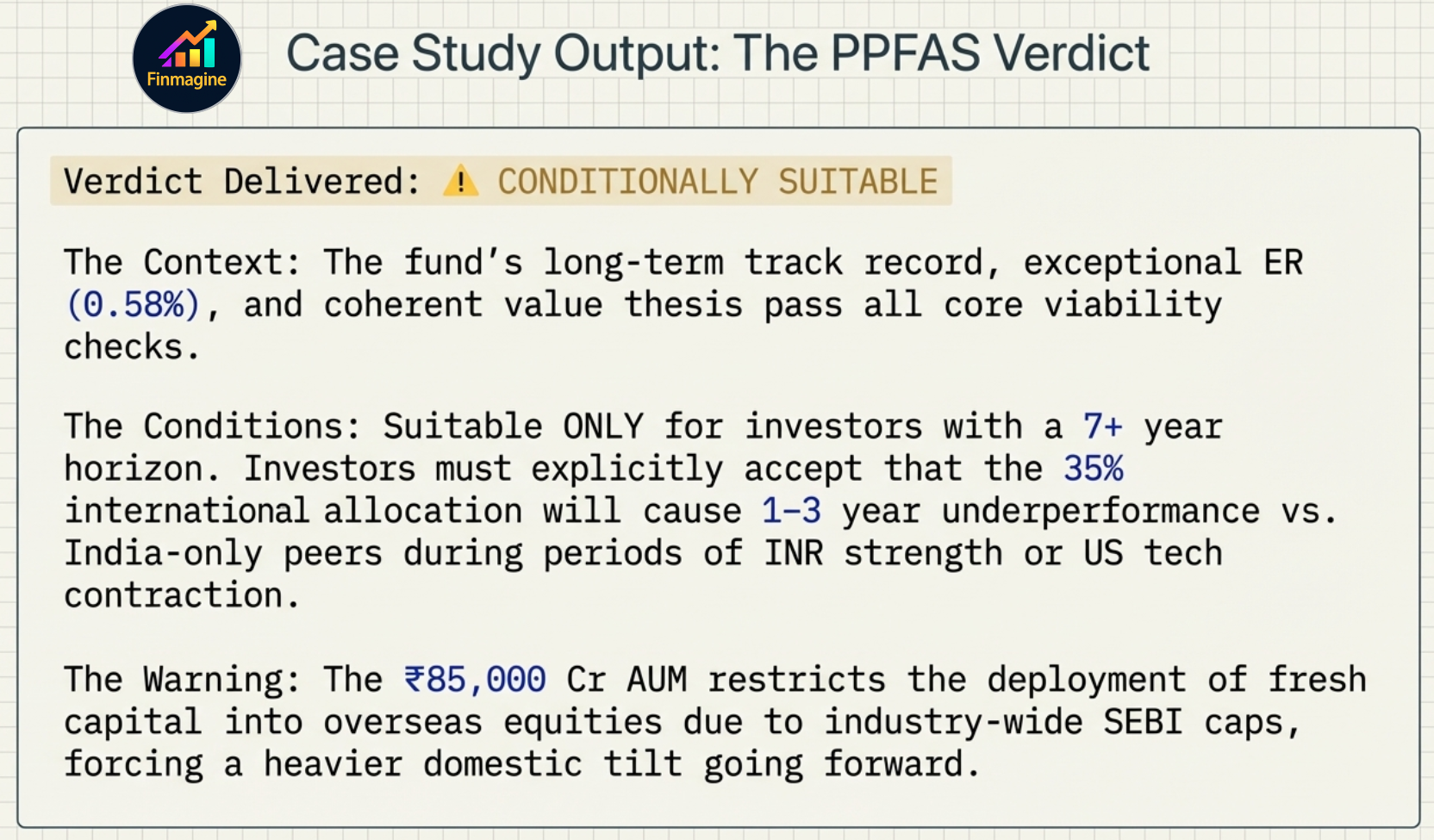

The PPFAS Case Study: Final Verdict

The AI's verdict on one of India's most celebrated funds: Conditionally Suitable — not because it is a bad fund, but because its success is mathematically beginning to constrain its future potential.

After synthesising all 7 dimensions, the AI delivers a verdict of Conditionally Suitable for PPFAS Flexi Cap Fund — Direct Plan. This is not a failure verdict. It is precisely the kind of nuanced, conditions-bearing output that separates a forensic analysis from a marketing brochure.

The conditions attached are explicit:

- Minimum 7-year time horizon required — the short-term international allocation volatility makes this unsuitable for investors with shorter horizons

- Accept cyclical underperformance — the fund will experience 1–3 year periods of significant underperformance versus pure Indian flexi cap peers whenever INR strengthens or US tech corrects. An investor who panic-sells during these windows will crystalise losses on a fund that was simply doing what its mandate requires

- Accept the AUM capacity ceiling — the era of explosive mid-cap alpha from PPFAS is structurally over. Future returns will be anchored more heavily by large-cap domestic stability and the constrained international allocation. Accept the mature fund, not the scrappy startup that built the original track record

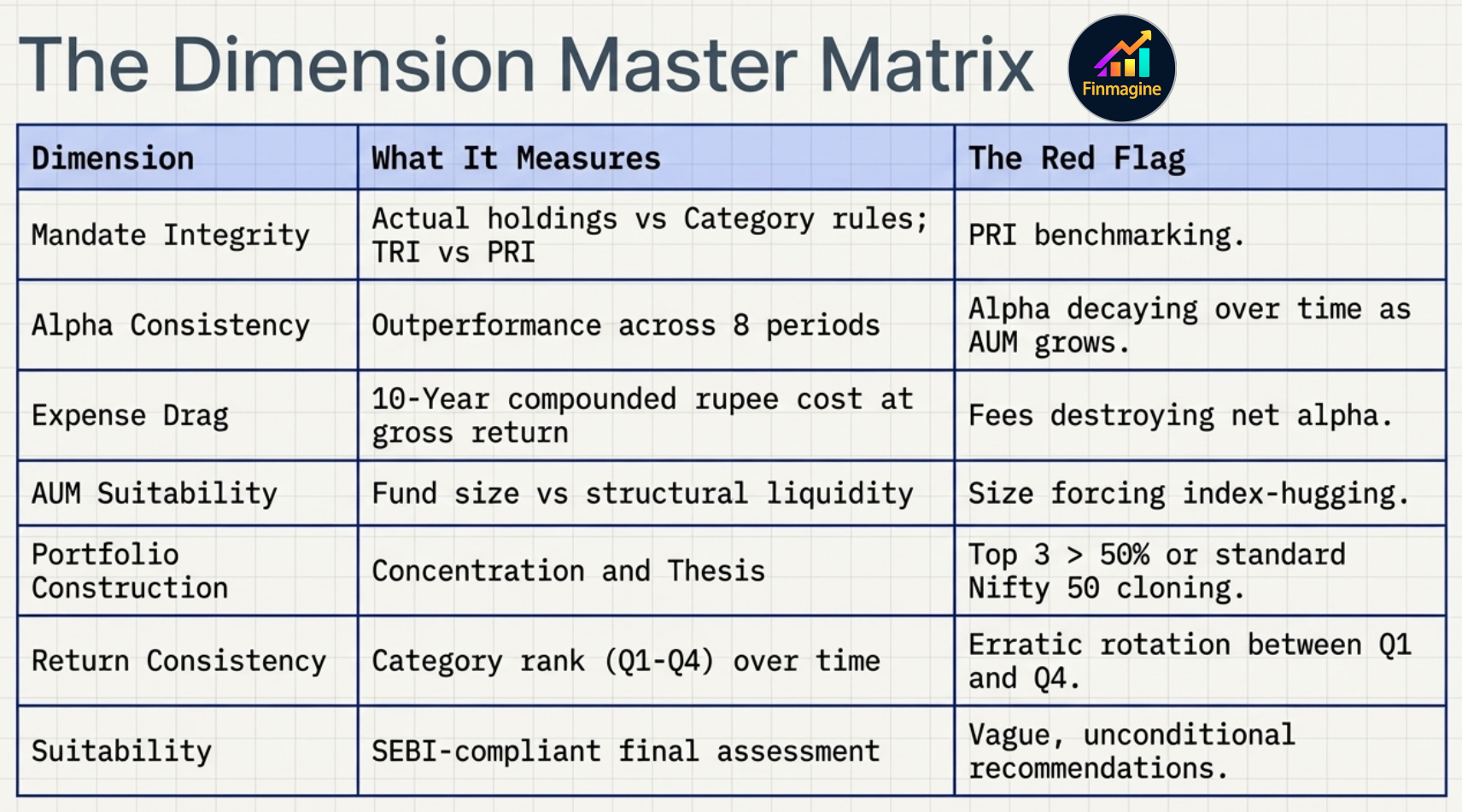

Quick Reference: The Dimension Master Matrix

Save this reference table — what each dimension measures, and the red flag that triggers a negative assessment.

| Dimension | What It Measures | The Red Flag |

|---|---|---|

| 1. Mandate Integrity | Actual holdings vs category rules; TRI vs PRI benchmark | PRI benchmarking; holdings outside stated category |

| 2. Alpha Consistency | Outperformance across all 8 periods | Alpha decaying over time as AUM grows (compression wedge) |

| 3. Expense Drag | 10-year compounded rupee cost at gross return | Fees destroying net alpha — investor subsidising the fund house |

| 4. AUM Suitability | Fund size vs structural liquidity of the mandate | Size forcing index-hugging; international cap hit for hybrid funds |

| 5. Portfolio Construction | Concentration and thesis clarity | Top 3 > 50% or standard Nifty 50 cloning (closet indexing) |

| 6. Return Consistency | Category rank (Q1–Q4) over time | Erratic rotation between Q1 and Q4; bottom quartile across periods |

| 7. Suitability Verdict | SEBI-compliant final assessment | Vague, unconditional recommendation — the AI must cite specific numbers |

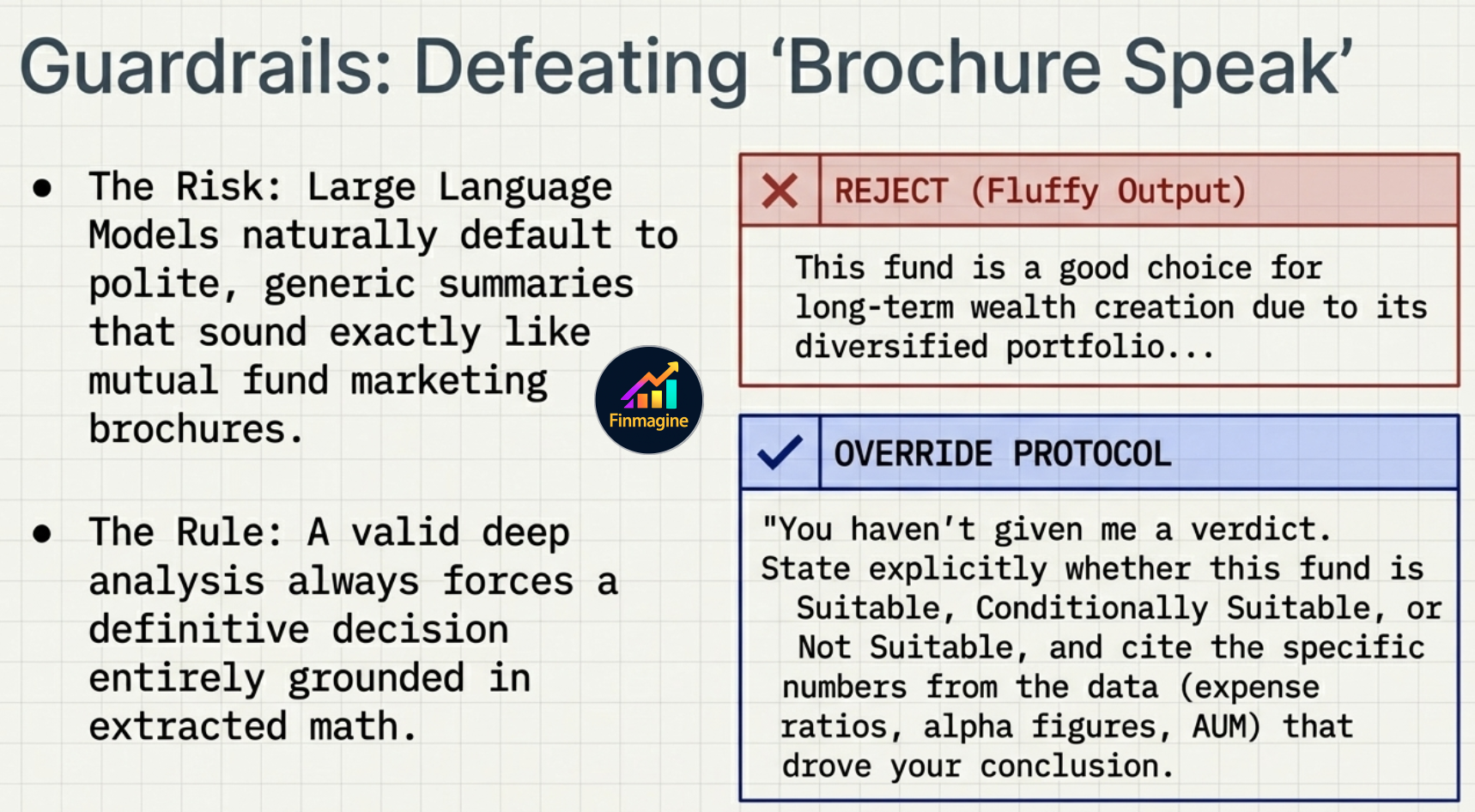

Guardrails: Defeating Brochure Speak

If the AI output sounds like a marketing brochure, use the override protocol — force a verdict with specific numbers.

Large language models are trained on the internet — which is saturated with glossy fund marketing materials. Their natural instinct is to default to the most common tone: polite, non-committal, and exactly as useful as the fund fact sheet you were trying to escape.

That is zero analytical value dressed as an expert opinion. It contains no numbers, no verdict, and no conditions.

"You haven't given me a verdict. State explicitly whether this fund is Suitable, Conditionally Suitable, or Not Suitable, and cite the specific numbers from the data — expense ratios, alpha figures, AUM thresholds, quartile ranks — that drove your conclusion. I need math, not adjectives."

A high-quality AI response to the Deep Analysis prompt looks like this: a clear stated verdict, specific extracted numbers supporting each claim (e.g. "10-year drag is ₹12,000 per lakh at 13% CAGR"), and falsifiable conditions attached to the verdict ("recommendation is conditioned on the fund manager remaining unchanged and AUM not exceeding ₹1,00,000 Cr"). If you do not get this, push back until you do.

Which AI to use: Claude is the top recommendation for Deep Analysis — unmatched at complex multi-dimensional reasoning, strict fee arithmetic, and delivering conditioned verdicts without fluff. ChatGPT is a strong alternate for Deep Analysis and Portfolio Fit. Gemini Deep Research is explicitly not recommended — its architecture compels it to search the web, corrupting the clean structured dataset the panel assembled.

Next in the Series

- Reading the Deep Analysis Output — How to interpret Suitable / Conditionally Suitable / Not Suitable in your actual investment decision, and when it is right to override the verdict

- Active vs Index: Does Your Fund's Alpha Justify Its Cost? — The template that gives you a direct Choose Active or Choose Index verdict

- Portfolio Fit: What to Write in the Context Box — Why vague context produces vague verdicts, and what the ideal context paragraph looks like

- ← Back to: Introducing MF Analysis on VRO

Run Your First Deep Analysis

Install Finmagine AI Advisor, open any mutual fund on Value Research Online, and generate a 7-dimension deep analysis in seconds. The SEBI suitability verdict is one click away.

Get Finmagine AI Advisor →Free Chrome Extension

Ready to try this yourself?

Install the Finmagine AI Advisor and generate institutional-grade research prompts from any Screener.in or stockanalysis.com company page in seconds.

Install from Chrome Web Store →No account required • Works on Chrome, Edge, Brave, Opera